The Rise of Lifestyle Hotels: What It Means for Independent Hotels

In Gen Z Checks In: The Rise of the Lifestyle Hotel, CBRE identifies lifestyle hotels as one of the fastest growing categories in global hospitality.

CBRE defines the category through three connected attributes: properties led by design and tied to their location, personalized service that avoids standardized delivery, and active public spaces that encourage social interaction.

A lifestyle hotel is not simply an aesthetic. It is a coherent idea expressed through design, service, shared spaces, operations, and a clearly defined target guest.

Many independent hotels already possess the characteristics larger groups are trying to reproduce. The work is to organize those strengths into a reliable guest experience and support it through clear positioning, distribution, and revenue management.

"A lifestyle strategy only works when the design promise, operating model, and guest mix all support the same business idea."

Independent Properties Already Have the Raw Material

Lifestyle hotels first emerged from independent boutique properties that created a stronger sense of place, distinctive design, and less standardized service. Larger hotel groups followed with acquisitions and new brands after seeing how travellers responded.

Independent hotels are not late to this idea.

A historic building, a restaurant known to local residents, genuine community ties, and staff who know repeat guests by name are difficult to reproduce through brand standards. These qualities are valuable only when they are visible, consistent, and relevant to the stay.

Character without clarity can be mistaken for inconsistency. Flexible space without a defined purpose may sit empty. A local identity has little effect on bookings when it is absent from the website, photography, room descriptions, arrival experience, and communication before the stay.

The opportunity is not to be different for its own sake. It is to turn what is already distinctive about the property into a clear promise that the team can deliver.

Supply Growth Is Moving Beyond Luxury

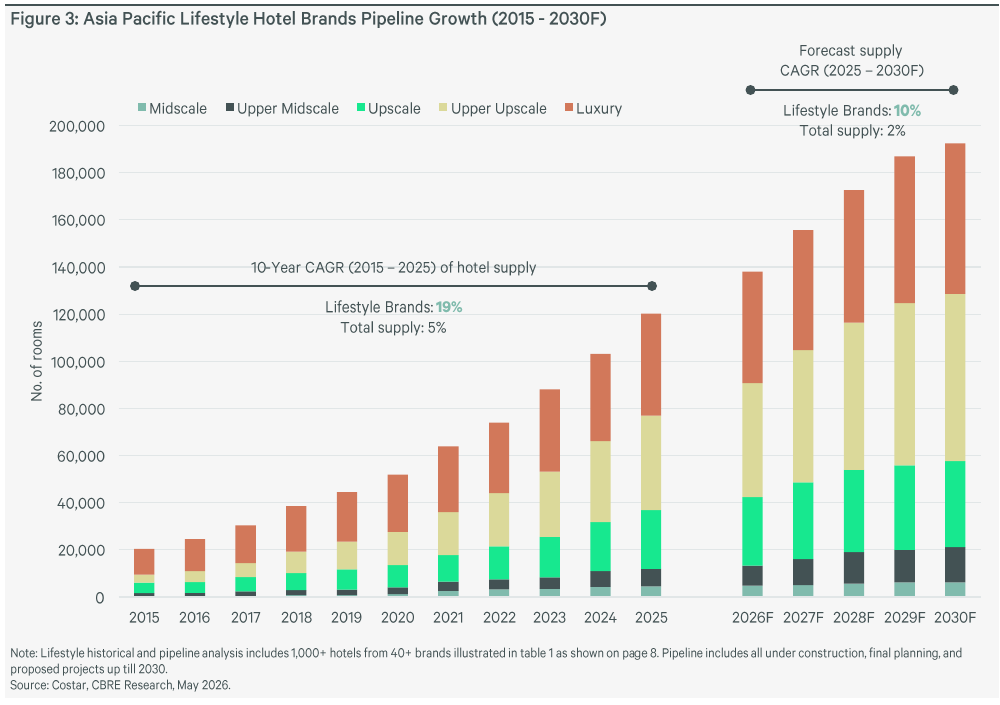

CBRE’s supply forecast shows how quickly branded lifestyle hotels have expanded across Asia Pacific. Lifestyle hotel supply grew at a compound annual growth rate of 19 percent from 2015 to 2025, while total hotel supply grew at 5 percent.

From 2025 to 2030, lifestyle supply is forecast to grow at 10 percent annually, compared with 2 percent for the broader hotel market. The chart also shows the category moving beyond luxury and upper upscale hotels into upscale, upper midscale, and midscale segments.

This matters for independent owners because a strong sense of place is not confined to expensive resorts or major city hotels. Smaller properties can express their identity without overreaching or committing to a major renovation.

In practical terms, improvements often begin with better room photography and clearer descriptions that explain why each room type suits a particular trip. They may also include a lobby that serves more than one purpose during the day, regional products within the breakfast or bar, and a booking journey that presents the property with confidence.

The strongest opportunity is often a clearer expression of what the property already has.

The Demand Signal Is About Experience

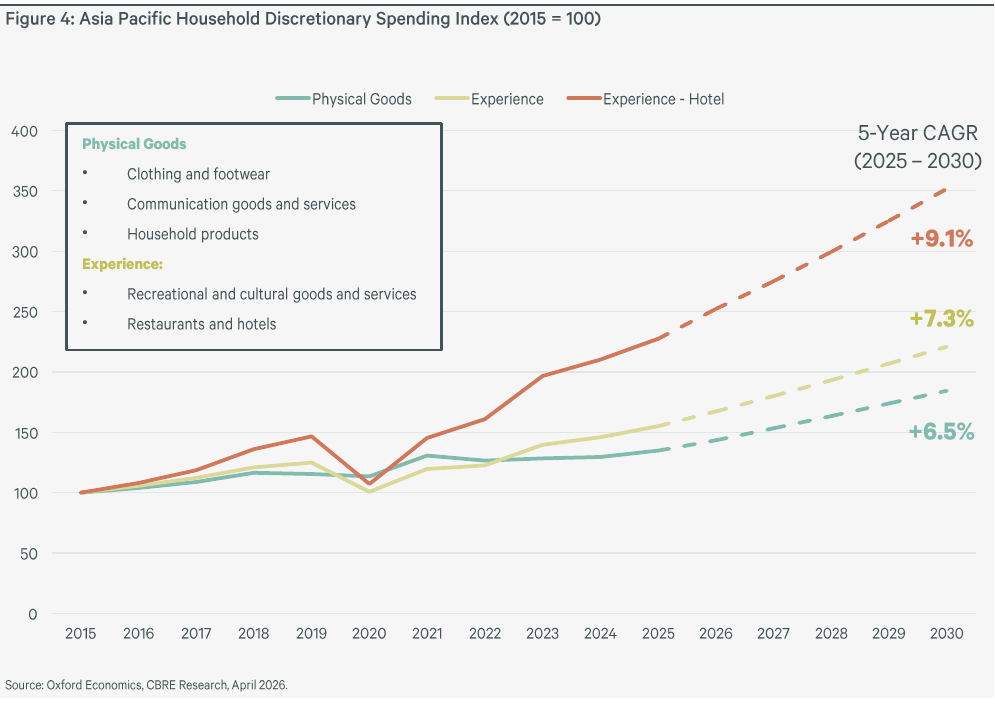

CBRE focuses on Gen Z because its spending power is rising and its hotel choices are less tied to traditional loyalty programs. The broader point is about growing demand for experiences.

The spending forecast below provides one of the clearest signals in the report. Experience spending in Asia Pacific is forecast to grow at 7.3 percent annually from 2025 to 2030, while spending on physical goods is forecast to grow at 6.5 percent. Hotel spending is forecast to grow faster, at 9.1 percent.

The figures are specific to Asia Pacific, but the operating question applies more widely: can a guest understand what the stay is for?

A clean, fairly priced room in a convenient location can still feel interchangeable. These fundamentals remain essential, but they rarely create preference on their own.

Independent properties can respond without adding unnecessary theatrics. The goal is to give guests a clearer reason to choose the property beyond price, location, and basic amenities. That reason may come from the building, the service, the atmosphere, or the property’s connection to its surroundings, but it must be clear before booking and credible after arrival.

Conversion Is One Path, Not the Only Path

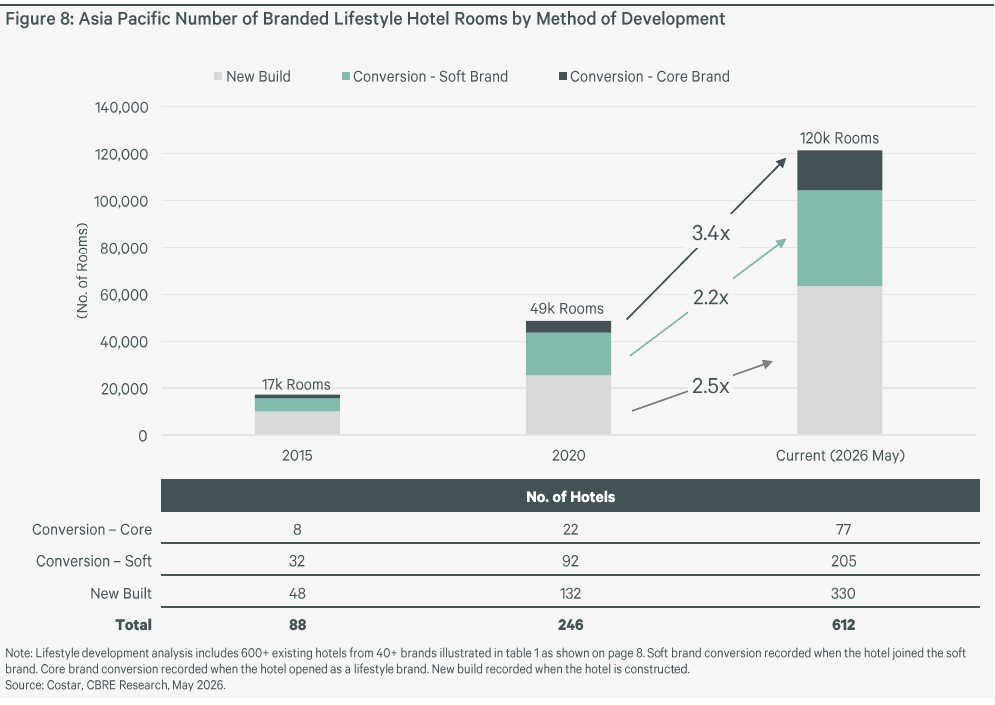

CBRE’s development data also shows the growing role of conversions. Branded lifestyle rooms in Asia Pacific increased from approximately 17,000 in 2015 to 120,000 by May 2026.

Soft brand conversions grew from 32 hotels to 205, while core lifestyle brand conversions grew from 8 hotels to 77. The chart reflects how existing properties are increasingly being repositioned rather than replaced through new construction.

Conversions can be an efficient use of capital when new construction costs are high.

Independent owners generally face three possible paths:

Remain Fully Independent

A fully independent property retains greater control over design, systems, partnerships, and positioning. It also retains responsibility for distribution, marketing, technology, and guest loyalty.

This can be the right approach when the hotel already has a clear identity, stable demand, and enough internal discipline to support its position.

Join a Soft Brand

A soft brand can provide access to wider distribution and loyalty programs while allowing the property to preserve more of its identity and operating flexibility.

The value depends on whether the additional reach and support justify the fees, requirements, and reduced control.

Convert to a Core Lifestyle Brand

A core lifestyle brand can provide stronger structure and wider recognition. It may also require more redesign, investment, and compliance with brand standards.

This approach may suit a property that needs a more substantial repositioning or ownership that wants a defined operating concept.

No single path is always best. The right decision depends on the market gap, asset condition, investment capacity, owner goals, and the specific problem the property is trying to solve.

Start With Positioning, Not Renovation

For most independent properties, the first step is an honest positioning review.

Begin with the guest. Identify the segments that already respond to the property and the segments the hotel can credibly serve next.

Then examine the entire guest journey. Photography, room descriptions, booking flow, arrival, public spaces, amenities, staff language, and follow up communication should reinforce the same idea.

Look for underused space and give it a clear role. A breakfast room can become a quiet work area by late morning. A lobby can support small community gatherings in the early evening. A modest outdoor area can become more useful through comfortable seating, lighting, and simple landscaping.

These changes do not require an elaborate concept. They require intent and a plan to maintain standards.

The revenue layer also needs attention. A clearer experience will not produce its full value if content remains weak, discounting is constant, and the channel mix is unmanaged.

Pricing should reflect the position of the property and the value of each room type. Distribution choices should match the guests being targeted. Technology should make booking and payment easier, reduce friction at arrival, and keep communication straightforward.

“Can the hotel explain why its rate is fair before the guest compares only room size and amenities?”

Practical adjustments often produce more value than large projects. Stronger presentation of room type differences, better use of the lobby throughout the day, relevant local partnerships, and enough staff authority to respond to guests are realistic steps that can improve both experience and revenue.

The Independent Hotel Opportunity

The growth of lifestyle hotels is not proof that travellers simply want fashionable properties.

It shows that identity, atmosphere, local connection, and purposeful shared spaces can influence guest choice and support rate.

Independent hotels often begin with many of these advantages. They do not need a lifestyle label or a fictional origin story to benefit. They need a clear position, consistent delivery, and an operating model capable of supporting the experience being promised.

Independent hotels do not need to become less independent. They need to become more intentional about what independence allows.